The Complete Financial Inventory Checklist for Indian Families

A category-by-category checklist of every account, policy and document an Indian family should track — plus the real, cited numbers on why so much of it quietly goes untracked.

By eKosha Team · · 5 min read

Every family has a financial life. Few families have a list of it. There’s a bank account here, a fixed deposit there, an old insurance policy someone bought years ago, a mutual fund folio nobody’s looked at since. None of it is lost, exactly — it’s just not written down anywhere the whole family can see.

That gap has a real, measured cost. As of March 2024, banks in India were holding ₹78,213 crore in deposits classified as unclaimed — accounts with no customer activity for ten years or more — up 26% from the year before, according to the Reserve Bank of India’s own data as reported by Business Standard. Add to that the crores sitting in inoperative EPF accounts, the roughly ₹20,062 crore in unclaimed life insurance payouts insurers were still holding as of March 2024, and shares and dividends sitting with the government’s Investor Education and Protection Fund Authority after seven years of no claims — and the picture is clear. This isn’t money that was stolen or mismanaged. It’s money whose existence nobody remembered to write down.

A financial inventory is simply the fix: one place that lists what your family owns, so nothing sits forgotten until a bank or regulator has to go looking for the rightful owner.

What a financial inventory actually is

It isn’t a budget, and it isn’t an investment plan. It’s simpler than both — a record of three things for every asset your family holds:

- What it is — the type of account, policy or asset.

- Where it lives — which bank, insurer or institution holds it.

- Who should know — the nominee on record, and the family member who can find it if needed.

Once that’s written down for everything you own, “being prepared” stops being an abstract idea and becomes a document you can actually hand someone.

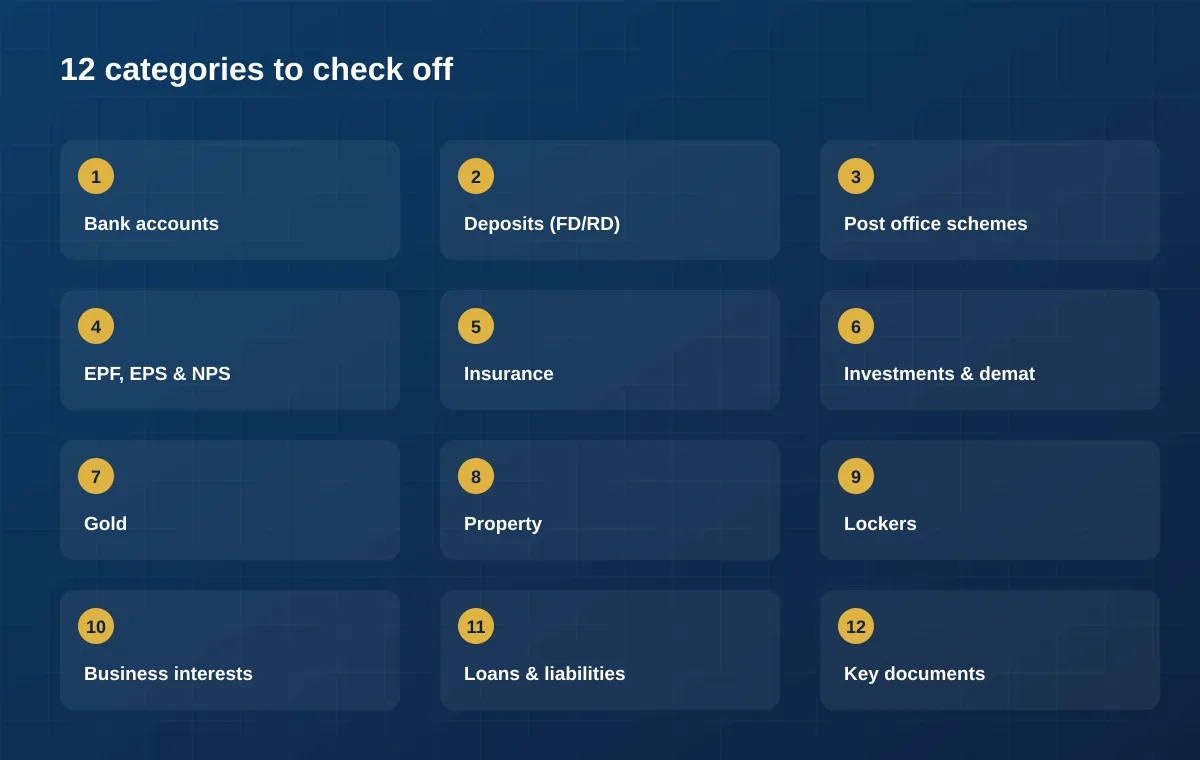

The checklist, category by category

Work through each section below. You don’t need every category to apply to your family — just capture what does, and note the institution, account or policy number, and current nominee for each item.

1. Bank accounts

Savings accounts, current accounts, salary accounts, and NRI accounts (NRE/NRO/FCNR) if any family member has lived abroad. Include accounts you rarely use — an old salary account from a previous job is exactly the kind of account that turns “unclaimed” after ten years of inactivity.

2. Deposits

Fixed deposits (FDs) and recurring deposits (RDs), across every bank — including small finance banks and co-operative banks, which families often forget once the FD receipt goes into a drawer.

3. Post office and small savings schemes

Public Provident Fund (PPF), National Savings Certificates (NSC), Kisan Vikas Patra (KVP), Senior Citizens’ Savings Scheme (SCSS), Sukanya Samriddhi accounts for daughters, and the ordinary Post Office Savings Account. These are especially easy to lose track of because they don’t send digital statements the way banks do.

4. Retirement and provident funds

Employees’ Provident Fund (EPF) and Employees’ Pension Scheme (EPS) balances from every employer you’ve worked for, and the National Pension System (NPS) if you contribute to one. Job changes are the single biggest reason EPF accounts go inoperative — an account is officially classified as inoperative after 36 months with no contribution or claim, per EPFO’s Standard Operating Procedure.

5. Insurance

Life insurance and term plans, health insurance (individual and family floater), motor insurance, and home insurance. Note the policy number, insurer, sum assured, and — critically — the nominee named on each policy.

6. Investments

Mutual fund folios, direct equity and demat accounts, and any PMS or AIF holdings. As of SEBI’s 2026 nomination framework, nomination is now mandatory by default on new single-holder demat accounts and mutual fund folios — a good reason to check that existing ones are actually nominated too.

7. Gold and precious metals

Physical gold and jewellery (and where it’s stored — locker, home safe), Sovereign Gold Bonds, gold ETFs, and digital gold holdings.

8. Property

Land and real estate, along with the title deed, registration papers, and property tax records for each. Note which family member currently holds the original documents.

9. Lockers

Bank lockers and their location, plus who is authorised to access them and under what conditions.

10. Business interests

Ownership stakes, partnership shares, or sole proprietorship assets, if applicable.

11. Loans and liabilities

Home loans, personal loans, credit cards, and any guarantees you’ve signed for someone else. A complete financial picture includes what’s owed, not just what’s owned — your family needs to know about liabilities just as much as assets.

12. Key documents

PAN, Aadhaar, passport, and where physical or digital copies of each of the above — passbooks, policy documents, property papers — are actually kept.

Making the list useful, not just complete

A checklist you fill in once and never touch again drifts out of date the moment you open a new account or close an old policy. The habit that matters more than the first pass is the second one: revisiting it whenever something changes, and making sure it’s somewhere more than one person can reach.

That’s the part most families skip — not because they don’t care, but because there’s never been an easy place to keep it. A shared spreadsheet gets outdated. A physical file lives in one drawer, in one house. Passwords to online accounts don’t get written down anywhere at all.

Where eKosha fits

This is exactly the gap eKosha is built to close. It’s a private, encrypted place to record this same checklist — every asset, its institution, and its nominee — and keep it current as your financial life changes.

With eKosha, you can:

- Record each asset across the categories that matter most — bank accounts, deposits, insurance, mutual funds and shares, gold, property, provident and pension funds, small savings, and lockers.

- Set nominees and co-owners on each one, so the record and the actual paperwork agree with each other.

- Share securely with the family members you trust, with view-only or edit access that you control and can change at any time.

Building the list is the hard part, and it only takes about fifteen minutes to start. Keeping it current is the part that protects your family — and that’s what eKosha is for.

Continue reading

Start organising what your family depends on

eKosha is free to start — add your assets, set your nominees, and share securely with the people you trust.

Get Started — it's freeGet preparedness tips in your inbox

Occasional, practical notes on organising your family’s finances. No spam, unsubscribe anytime.